Investor's Corner

What to look for in Tesla Motors Q1 Financials

Tesla (NASDAQ: TSLA) is set to announce its first quarter earnings report after market close on Wednesday, May 4, 2016.

TSLA reported 4th quarter 2015 earnings of $ -0.87 per share on February 10, 2016. This missed the consensus of $ 0.10 by $ -0.97 of the 16 analysts covering this company. Interestingly that turned out to be the end of a dramatic 42% slide which began on January 1st. Since then TSLA has moved from its lowest point of $141 on that day to roughly $250 per share, a 78% increase in just 3 months. That kind of tells you that TSLA is a stock not for the faint of heart.

Source: WallSt I/O

The consensus of the 14 analysts covering TSLA for 1st quarter 2016 is a per share loss of $ -.57, with range estimates of: 0.080 | -0.569 | -1.000 (High | Mean | Low).

")

$TSLA earnings summary via E-Trade

Based on 20 analysts offering 12-month targets from TSLA, the average price target is $243.95, effectively a zero-move from the current stock price. If you are an “investor” in TSLA stock, the pros tell you that TSLA will not go anywhere in the next 12 months.

$TSLA analysis via TipRanks

So those are the numbers from the pros, but if you still decide that you want to trade TSLA stock, what should you be looking for in the quarterly results and the conference call webcast?

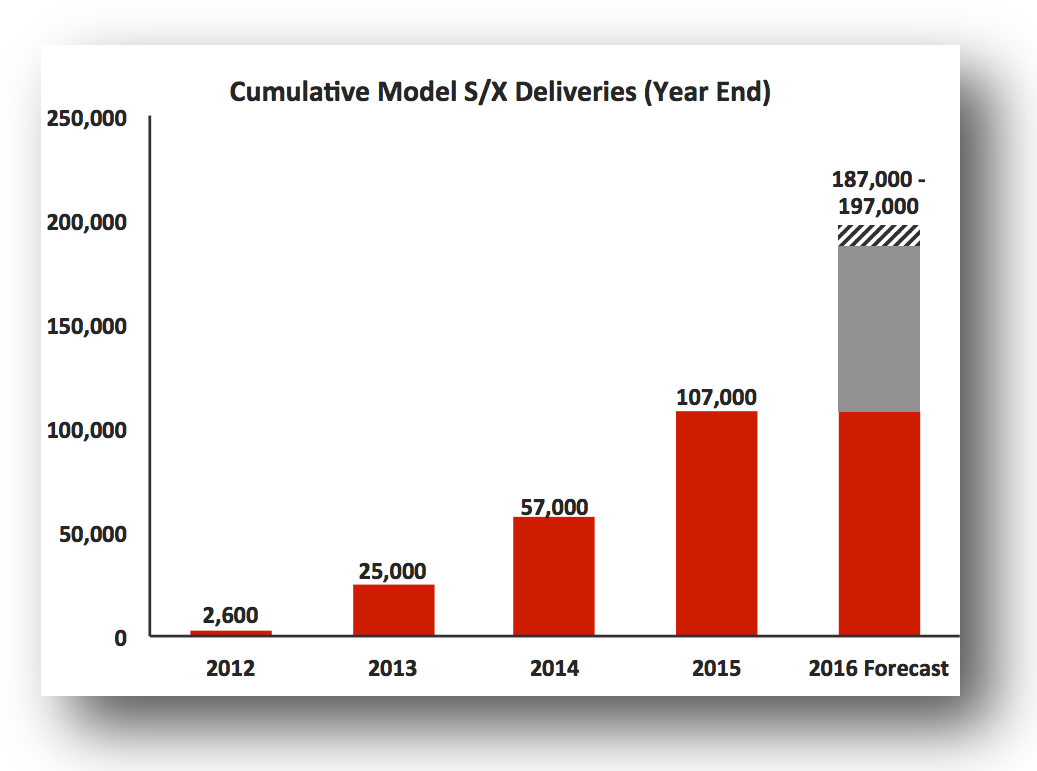

Q1 Vehicle Deliveries

Let’s take a look at a few items from the “Tesla 4th Quarter & Full year 2015 Shareholder Letter”.

In the “Q1 and Full Year 2016 Outlook” section, Tesla states that “we plan to deliver 80,000 to 90,000 new Model S and Model X vehicles in 2016. […] In Q1, we plan to grow deliveries 60% year on year to approximately 16,000 vehicles”.

Source: Tesla Motors

We already know that Q1 deliveries did not meet the promised 16,000 units, as that number was actually 14,820, due to “severe Model X supplier parts shortages in January and February” as provided in a Press Release on April 4, 2016. In the same release, “Tesla reaffirms its full-year delivery guidance [of 80,000 to 90,000 vehicles].”

The missing income due to the delayed Model X vehicles delivery will be partially offset by the initial Model 3 “reservations”. It is quite interesting that reservations opened on March 31, 2016, the last day in the quarter, and at least 125,000 of them may be counted as an additional $125M income in Q1. In the end, guidance on vehicle deliveries for Q2 2016 will be one of the deciding factors on where TSLA stock moves post the Q1 report.

Cash Flow and Margins

In the same Q4 Shareholder Letter, Tesla states that “we expect to generate positive net cash flow and achieve non-GAAP profitability for the full-year 2016”, and “we plan to fund about $1.5 billion in capital expenditures without accessing any outside capital.” These are both very aggressive goals, especially in light of the 400,000+ Model 3 reservations, as of the latest disclosed counts. Elon Musk has already tweeted that he is “definitely going to need to rethink production plans”, which likely means that another factory will be needed to produce the Model 3 in a reasonable timeline that will allow delivery to the majority of the current reservation holders. This more aggressive delivery of Model 3 vehicles as originally envisioned will likely require outside capital for building such factory.

Definitely going to need to rethink production planning…

— Elon Musk (@elonmusk) April 1, 2016

Since missing the mark on Model X will impact cash flow for Q1, I would expect questions in the conference call asking if the issues have been resolved, and if the missing Model X numbers can be made up in Q2. While cash flow reversed action to the positive for the first time during Q4 2015, with a strong $179M cash flow from core operations, Tesla needs to prove that this behavior will continue in 2016.

Again in the Q1 Shareholder Letter, Tesla states that “Throughout the rest of 2016, Automotive gross margins should continue to increase. […] Model S gross margins should begin to approach 30% and Model X gross margins should be about 25%.” In Q4 gross margins were 20.9% for the Tesla Model S and even a slight increase in margins will be viewed positively by the market. This is a number that will be greatly watched as Tesla needs to prove that it can eventually deliver 500K+ vehicles / year at a profit. Much of the current valuation of Tesla stock is built on this assumption. Accordingly, a drop in margins for Q1 would be viewed very negatively by the market, at least for the short term.

Summarizing, besides vehicle delivery, cash flow and margins will be the other two drivers of the TSLA stock short-term market action after the Q1 report numbers are released.

Live Q&A Webcast

Tesla management will hold a live question & answer webcast on May 4 at 2:30pm Pacific Time to discuss the Company’s financial and business results and outlook. Live and replay webcast will be available at http://ir.teslamotors.com/eventdetail.cfm?EventID=171952 .

Tip of the Week

Starting with today’s posting I’ll be including a “tip of the week.” This may involve covering a trading concept, or recommending a website with tools or information useful to investors and traders of TSLA.

For this week, I am recommending signing up for the free Basic Membership of TipRanks. With it you can receive free alerts for 1 stock and 1 expert, which is enough for the ones just interested in TSLA stock. Happy trading.

Disclosure: I currently have no positions in any stocks mentioned, but I may plan to initiate positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Teslarati). I have no business relationship with any company whose stock is mentioned in this article.

A recent 13-F filing from legendary investor and billionaire Ray Dalio’s Bridgewater Associates has revealed that the hedge fund has added over $62 million worth of Tesla stock (NASDAQ:TSLA) to its portfolio.

Elon Musk has praised the billionaire’s investment in a post on X.

Bridgewater’s TSLA stake:

- As per Bridgewater’s 13-F filing, it currently holds 153,589 shares of TSLA, which costs $62,025,382.

- The firm added the TSLA shares in the fourth quarter.

- Tesla shares gained momentum after its Q3 2024 earnings call, and it only gained more strength after the election of U.S. President Donald Trump.

- At the end of 2024, Tesla shares were up 62%, as noted in a MarketWatch report.

- Tesla stock is still up 88% over 12 months despite a steep drop over the past month.

Smart move

— Elon Musk (@elonmusk) February 14, 2025

A vote of confidence:

- Bridgewater Associates is one of the largest hedge funds in the world, so the firm’s stake in TSLA could be interpreted as a vote of confidence in the electric vehicle maker.

- Elon Musk has praised the firm’s investment. In a post on X, Musk noted that Bridgewater’s investment was a “smart move.”

- Elon Musk has been quite consistent on his idea that Tesla could eventually become the world’s most valuable company. He emphasized this point during the Q4 2024 earnings call.

- “I see a path. I’m not saying it’s an easy path but I see a path of Tesla being the most valuable company in the world by far. Not even close. There is a path where Tesla is worth more than the next top five companies combined,” Musk said.

Don’t hesitate to contact us with news tips. Just send a message to simon@teslarati.com to give us a heads up.

Tesla shares (NASDAQ:TSLA) have received a “Buy” rating and a $475 per share price target from Benchmark.

Benchmark’s price target is based on 68.2 times its 2028 earnings before interest, taxes, depreciation, and amortization (EBITDA), as noted in a Morningstar report.

Tesla rating:

- In a note to clients, Benchmark analyst Mickey Legg noted that Tesla has outlined a path towards more growth through several of its initiatives.

- These include Tesla’s work in autonomous driving systems, robotics, and energy generation.

- The company could also make more headway into the electric vehicle segment.

- “The company has outlined a path for growth with a more affordable vehicle scheduled for 1H25, unsupervised full self-driving as a paid service this June in Austin, TX, and Optimus robot production ramp through 2026 and beyond,” the analyst stated.

$TSLA +1.8% pre-mkt as Benchmark initiates TSLA with a Buy rating and $475 price target. pic.twitter.com/KT6BTTW5kJ

— Gary Black (@garyblack00) February 12, 2025

More potential:

- While he sees potential in Tesla, the Benchmark analyst noted that his current model only incorporates vehicle growth.

- Thus, there could be “significant potential upside” if the company’s autonomous vehicle program and Optimus are scaled.

- “Tesla’s market leadership, near-term catalysts, strong management, and diversified business justify the stock’s market premium,” Legg noted.

Don’t hesitate to contact us with news tips. Just send a message to simon@teslarati.com to give us a heads up.

Investor's Corner

Tesla is ‘better-positioned’ as a company and as a stock as tariff situation escalates

Tesla is “better-positioned” as a company and as a stock as the tariff situation between the United States, Mexico, and Canada continues to escalate as President Donald Trump announced sanctions against those countries.

Analysts at Piper Sandler are unconcerned regarding Tesla’s position as a high-level stock holding as the tariff drama continues to unfold. This is mostly due to its reputation as a vehicle manufacturer in the domestic market, especially as it holds a distinct advantage of having some of the most American-made vehicles in the country.

Analysts at the firm, led by Alexander Potter, said Tesla is “one of the most defensive stocks” in the automotive sector as the tariff situation continues.

The defensive play comes from the nature of the stock, which should not be too impacted from a U.S. standpoint because of its focus on building vehicles and sourcing parts from manufacturers and companies based in the United States. Tesla has held the distinct title of having several of the most American-made cars, based on annual studies from Cars.com.

Its most recent study, released in June 2024, showed that the Model Y, Model S, and Model X are three of the top ten vehicles with the most U.S.-based manufacturing.

Tesla captures three spots in Cars.com’s American-Made Index, only U.S. manufacturer in list

The year prior, Tesla swept the top four spots of the study.

Piper Sandler analysts highlighted this point in a new note on Monday morning amidst increasing tension between the U.S. and Canada, as Mexico has already started to work with the Trump Administration on a solution:

“Tesla assembles five vehicles in the U.S., and all five rank among the most American-made cars.”

However, with that being said, there is certainly the potential for things to get tougher. The analysts believe that Tesla, while potentially impacted, will be in a better position than most companies because of their domestic position:

“If nothing changes in the next few days, tariffs will almost certainly deal a crippling blow to automotive supply chains in North America. [There is a possibility that] Trump capitulates in some way (perhaps he’ll delay implementation, in an effort to save face).”

There is no evidence that Tesla will be completely bulletproof when it comes to these potential impacts. However, it is definitely better insulated than other companies.

Need accessories for your Tesla? Check out the Teslarati Marketplace:

- https://shop.teslarati.com/collections/tesla-cybertruck-accessories

- https://shop.teslarati.com/collections/tesla-model-y-accessories

- https://shop.teslarati.com/collections/tesla-model-3-accessories

Please email me with questions and comments at joey@teslarati.com. I’d love to chat! You can also reach me on Twitter @KlenderJoey, or if you have news tips, you can email us at tips@teslarati.com.

Tesla Model Y tops South Korea import sales in February 2025

Elon Musk companies under scrutiny in the EU

Hyundai dives into the robotaxi business with TX-based startup

-

News1 day ago

News1 day agoSpaceX announces Starship Flight 8’s new target date

-

News2 days ago

News2 days agoTesla launches fresh U.S. promotions for the Model 3

-

Elon Musk3 days ago

Elon Musk3 days agoTesla mulls adding a new feature to fight off vandals as anti-Musk protests increase

-

News4 days ago

News4 days agoTesla’s lead designer weighs in on plans for these two Model Y colors

-

News3 days ago

News3 days agoTesla starts Model Y ‘Launch Edition’ deliveries in the U.S.

-

Elon Musk3 days ago

Elon Musk3 days agoTesla gaining with Republicans as it loses traction with Democrats: Stifel

-

Energy19 hours ago

Energy19 hours agoTesla lands in Texas for latest Megapack production facility

-

News2 days ago

News2 days agoTesla China wholesale figures drop in February amid new Model Y transition